Constant Marginal Costs Occur When Each Individual Unit Costs

In economics the marginal cost is the change in the total cost that arises when the quantity produced is incremented the cost of producing additional quantity. Marginal costs are important because economic decisions are made at the margin.

/producer_surplus_final-680b3c00a8bb49edad28af9e5a5994ef.png)

Producer Surplus Definition

More than the next one.

. In practice however marginal cost is measured by the total variable cost attributable to one unit. As Figure 1 shows the marginal cost is. For example if producing two clocks costs 4 and producing one costs 350 the companys marginal cost for producing two clocks is 050.

The variable cost per unit is a constant value. The business then produces at additional 100 units at a cost of 90. When will a firm find the.

Less than the marginal cost an activity should be reduced. The difference is marginal cost for two units. B more than the previous one.

The average cost of producing 100 units is 2 or 200 100. Divided by the change in quantity which is the additional 100 units. More than the previous one.

Which of the following occurs when the long-run average cost of producing each individual unit increases as total output increases. Assumptions in marginal costing. For example the economic decision of a physician practice to expand or reduce a particular service in response.

A constant cost industry is an industry where each firms costs arent impacted by the entry or exit of new firms. 90100 which equals 090 per unit as the marginal cost. This can be made clear with the help of diagram 13.

Servicing one additional customer would cost 2000. This is the currently selected item. Costs are either fixed or variable costs.

When a decision maker makes a quick decision without taking the time to compare the opportunity cost of all possible options he is using. However the marginal cost for producing unit 101 is 4 or 204 - 200 101-100. B Fixed costs are considered period costs and are not included in product cost only variable costs.

Constant marginal costs occur when each individual unit costs. 2 Constant marginal costs occur when production of each individual unit costs. Constant marginal cost is the total amount of cost it takes a business to produce a single unit of production if that cost never changes.

The main features of marginal costing are as follows. In this example marginal costs for various activities exist. When charted linearly a marginal cost trends.

Select the correct answer below. Less than the previous one to produce. This is illustrated in Figure 1310.

Less than the previous one. TC Q a b Q. It is calculated by taking the total cha.

Marginal cost is the variable cost per unit. The same to produce as the previous one. A less than the previous one.

O economies of scale diseconomies of scale O. So the marginal cost would be the change in total cost which is 90. The main uses are.

61Constant marginal costs occur when production of each individual unit costs. March 14 2022 Constant marginal cost is the total amount of cost it takes a business to produce a single unit of production if that cost never changes. Iii Law of Constant Returns or Constant Costs.

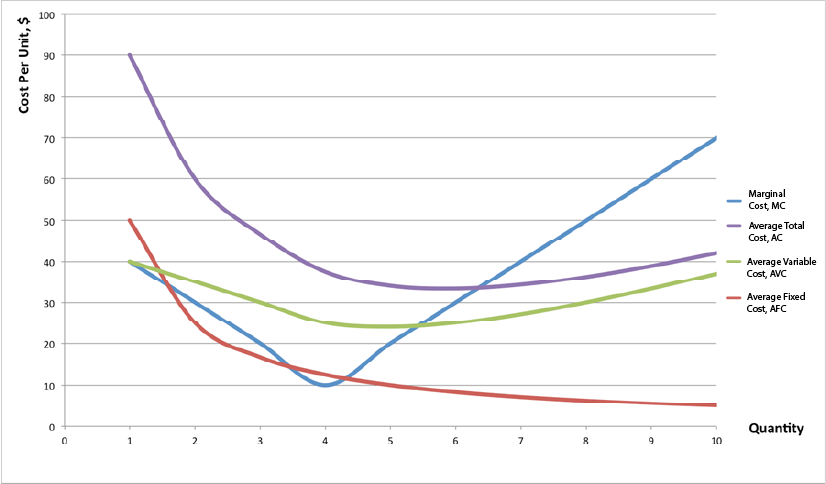

Where the marginal costs would be 1005. In some contexts it refers to an increment of one unit of output and in others it refers to the rate of change of total cost as output is increased by an infinitesimal amount. Q Total Cost TC Marginal Cost MC Average Cost AC 1 10 10 10 2 16 6 8 3 23 7 76 4.

For example let us suppose. According to the law of constant returns when a firm employs more and more factors output increases at a constant rate. Variable cost per unit is same at any level of activity.

42 which is just a constant. 3 The costs associated with variable inputs are ____ and the costs associated with ___ inputs are ____. This might occur if the firm has a high fixed cost and constant marginal costs leading to declining average total costs for all levels of output.

A All costs are categorized into fixed and variable costs. Marginal cost is the increment in cost that occurs when the output produced is increased by one unit. In marginal costing fixed production overheads are not absorbed into products costs.

The total cost of producing 101 units is 204. That is it is the cost of producing one more unit of a good. In this case a single firm will be able to produce a given level of output at a lower average cost than two or more firms because a single firm only has to incur the fixed cost once whereas multiple firms.

Marginal cost is the change in the total cost when the quantity produced is incremented by one. The same to produce as the previous one. More than the previous one to produce.

The marginal cost for one additional unit produced is either 5 for any unit except the 101 st 201 st etc. In this situation increasing production volume causes marginal costs to go down. Economics questions and answers.

Marginal Cost Change in Costs Change in Quantity Marginal cost represents the incremental costs incurred when producing additional units of a good or service. Constant marginal costs occur when each individual unit costs A. Marginal Cost Calculator This marginal cost calculator allows you to calculate the additional cost of producing more units using the formula.

The total cost per hat would then drop to 175 1 fixed cost per unit 075 variable costs. Definition of Marginal Cost Marginal Cost is the cost of producing an extra unit. Fixed costs remain constant in total regardless of changes in volume.

The marginal cost of introducing a new product line would be 10000. Let us say that Business A is producing 100 units at a cost of 100. DTC Q dQ b.

Planning forecasting and decision making. It is the addition to Total Cost from selling one extra unit. In the previous lesson when we used a constant heat rate to derive.

Fixed cost are costs that remain same in total in each period. Although total variable cost may increase or decrease consequent upon increase or decrease in output variable cost per unit remains constant for all levels of output within the installed capacity. Therefore the average cost curve as well as marginal cost curve remains parallel to horizontal axis.

41 where TC is total cost Q is total output MWh and a and b are constants then the marginal cost of electricity production is found by taking the derivative of the total cost function. There are several ways to measure the costs of production and some of these costs are related in interesting waysFor example average cost AC also called average total cost is the total cost divided by quantity produced. Variable cost per unit Rs 25 Fixed cost Rs 100000 Cost of 10000 units 25 10000 Rs 250000 Total Cost of 10000 units Fixed Cost Variable Cost 100000 250000 Rs 350000.

More formally it is the derivative of the total cost function with respect to output. Since the cost is the same for every single unit produced it is considered. The same as the previous one.

Learn about the difference between the short run market supply curve and the long run market supply curve for perfectly competitive firms in constant cost industries in this video. Marginal cost MC is the incremental cost of the last unit produced.

Long Run Supply When Industry Costs Aren T Constant Video Khan Academy

Marginal Costs An Overview Sciencedirect Topics

Economies Of Scale Microeconomics

Increasing Marginal Costs And The Efficiency Of Differentiated Feed In Tariffs Sciencedirect

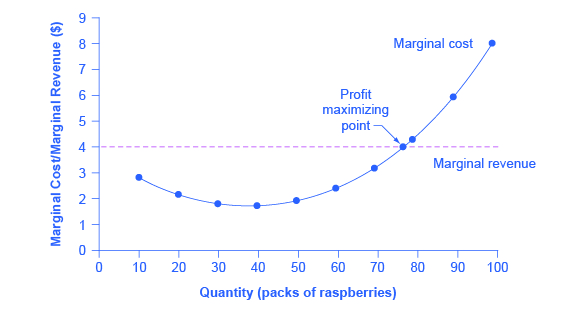

8 2 How Perfectly Competitive Firms Make Output Decisions Principles Of Economics

The Law Of Diminishing Marginal Returns Economics Help

The Firm Under Competition And Monopoly

Costs Of Production Maple Help

Diagrams Of Cost Curves Economics Help

Module 8 Cost Curves Intermediate Microeconomics

Costs Of Production Economics Help

/MinimumEfficientScaleMES2-c9372fffba0a4a1ab4ab0175600afdb6.png)

Minimum Efficient Scale Mes Definition

8 2 How Perfectly Competitive Firms Make Output Decisions Principles Of Economics

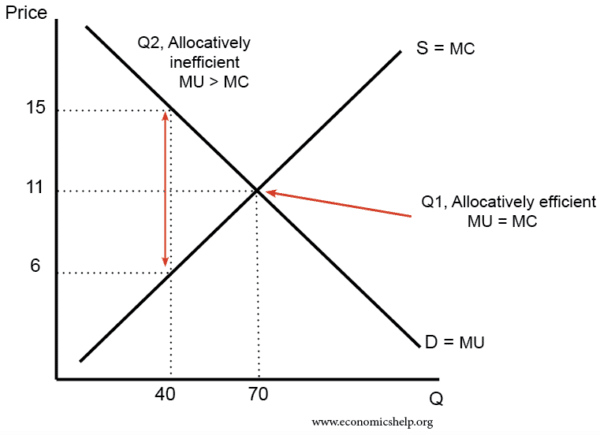

Marginal Utility Theory Economics Help

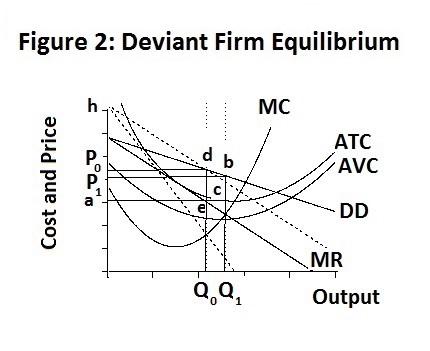

Duopoly Cournot Nash Equiibrium

Duopoly Cournot Nash Equiibrium

Marginal Utility Theory Economics Help

Micro Chapter 8 Perfect Competition Flashcards Quizlet

/MarginalRateofSubstitution3-a96cfa584e1440f08949ad8ef50af09a.png)

Marginal Rate Of Substitution Mrs Definition

Comments

Post a Comment